Accounting Basics – What is the Accounting Cycle?

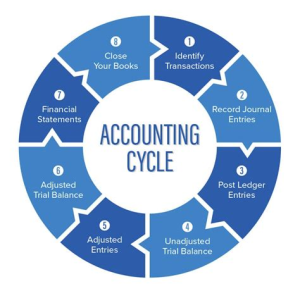

The accounting cycle is a step-by-step process used by businesses to record their transactions and prepare financial documents. It’s recommended that businesses use double-entry accounting, but you can use any method that works for your business. The first step is to set up a trial balance. The objective of a trial balance is to catch errors during the first stage of the accounting cycle. If the debit and credit account balances are equal, the trial balance is considered successful. The next step is to verify the trial balance for mistakes.

The next step is to gather all the transaction information throughout a period. In order to create an accurate financial statement, you will need to know how to calculate all of the expenses and income. Once these accounts are calculated, you can construct the balance sheet and income statement. Then you will need to prepare the cash flow statement and the final balance sheet. To learn more about the accounting cycle, consult with Swindon Accountants such as Chippendale and Clark Accountants in Swindon.

Another part of the cycle, you need to keep records of all of the transactions in what is known as bookkeeping. During this step, you’ll record all of the transactions into your company’s books of accounts. A general ledger will contain two tables for capital and cash. The closing balance will be transferred to these accounts. These things can seem complicated to the inexperienced which is why many businesses rely on the services of an accountant.

{kind=link}

{kind=link}

{kind=link}